How Much Is Gap Insurance Monthly? Shocking Cost Breakdown

Ever wondered what gap insurance actually is and why so many drivers pay for it? In this blog, you’ll discover exactly what gap insurance does, why your regular car insurance sometimes falls short, how it’s priced, where you can buy it, and whether it’s actually worth paying for all explained in a way that even a 5-year-old can understand.

Gap Insurance Monthly? costs around $20 to $40 per month, depending on your car, loan, and insurer. In this guide, we’ll break down these numbers and help you decide if gap insurance is the right choice for you with real-life examples and a super-easy checklist at the end.

What Is Gap Insurance and Why Do People Pay for It?

Imagine you buy a brand-new car for $30,000. You drive it for a few months, and suddenly, it gets totaled in an accident. Your car insurance says, “We’ll pay you $24,000 that’s what your car is worth now.” But wait… you still owe $28,000 on your car loan! That $4,000 difference? That’s the gap. And gap insurance is what helps you cover that gap so you don’t have to pay from your own pocket.

People pay for gap insurance because cars lose value fast much faster than most people pay off their loans. If your car gets wrecked or stolen, and you still owe money, your regular car insurance won’t cover that leftover loan. Gap insurance steps in to save the day. It’s like a safety net for your wallet when the worst happens.

What does gap insurance really do for your car?

Imagine buying a new toy car. It’s shiny and expensive, and you love it. But what if it breaks and you can’t fix it? And you still owe money for it. That’s where gap insurance helps.

Gap insurance helps when your car gets totaled or stolen. Your regular insurance might not cover the full loan or lease amount.

Let’s say your car’s value is $15,000, but you owe $20,000. Your insurance will only give you $15,000. You’ll have to pay the extra $5,000 yourself. That’s the “gap.”

Gap insurance pays that extra $5,000 for you. It saves you from a big financial burden. That’s why many people, especially those with new cars and big loans, get it.

Why isn’t regular car insurance enough sometimes?

Many think, “I already have car insurance, I’m covered!” But regular car insurance only pays for your car’s current value. It doesn’t cover what you still owe.

Let’s look at an example:

- You bought a new car for $25,000.

- After a year, its value drops to $18,000.

- You still owe $22,000 on your loan.

If your car gets totaled, your insurance pays $18,000. But you owe $22,000. That’s a $4,000 gap. You’ll have to pay that extra money yourself, unless you have gap insurance.

So, regular car insurance doesn’t consider your loan. It only looks at your car’s current value. That’s why it’s not always enough if you’re still paying off your car.

So, How Much Does Gap Insurance Cost Each Month?

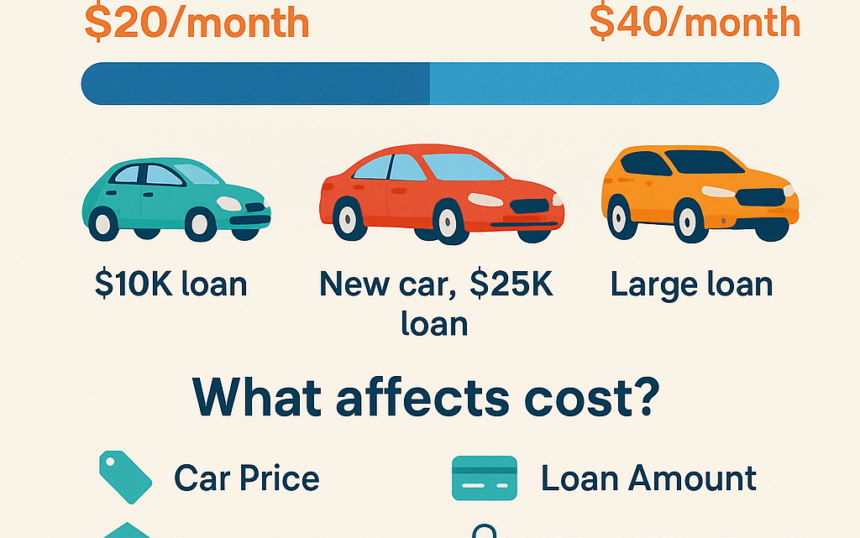

Let’s get straight to the point gap insurance usually costs between $20 to $40 per month. But this price isn’t the same for everyone. It depends on things like what kind of car you drive, how much money you borrowed to buy it, and who your insurance company is.

Think of it like this: if you buy an expensive car with a big loan, your gap insurance might cost more. But if your car is cheaper or your loan is small, it could cost less. Also, if you add gap insurance to your regular car insurance policy, it’s often cheaper than buying it from a car dealer.

It’s kind of like buying a toy with batteries. The more features the toy has (like sounds and lights), the more batteries it needs. Same with gap insurance the more your situation needs protection, the more it might cost each month.

Average monthly cost of gap insurance explained in kid-friendly terms

Now, let’s talk about money. Gap insurance costs about $20 to $40 per month. Sometimes it’s cheaper, sometimes more. We’ll explain why in the next section.

Think of it like this: every month, you give a little money to protect yourself from a big loss later. It’s like paying a few dollars now to save thousands if something bad happens to your car.

Some people get gap insurance for a one-time fee, like $300 to $600 when they buy the car. But if you pay monthly, it’s usually about the cost of a big pizza per month 🍕

What makes gap insurance cheaper or more expensive?

Great question The price of gap insurance depends on a few things. Let’s break them down like building blocks:

- Your Car’s Value: If you bought an expensive car, gap insurance might cost more because it has to cover a bigger “gap.”

- Loan or Lease Amount: If you took a big loan (and especially if you didn’t make a down payment), the “gap” can be larger which means gap insurance will cost a bit more.

- Where You Buy It: Buying gap insurance from a dealer usually costs more than getting it from your car insurance company. Dealers often charge a flat one-time fee, while insurers let you pay monthly.

- Insurance Provider: Some insurance companies offer cheaper gap coverage than others. It’s like how some ice cream shops charge more than others same idea, different price.

- Your Location: Where you live can also matter. Some places have higher car theft or accident rates, so gap insurance might cost a bit more there.

So in short: bigger loan + expensive car + buying from dealer = more expensive gap insurance. But smaller loan + buying from insurance company = usually cheaper.

Where Can You Buy Gap Insurance and How Is It Charged?

When you’re ready to buy gap insurance, you’ll usually have two main places to choose from: your car dealership or your car insurance company. Both can give you gap coverage, but they work in different ways.

Can I get gap insurance from my car dealer or my insurance company?

Yes, you can get it from either one but they offer it differently:

If you’re at the dealership, they might offer you gap insurance as a one-time add-on when you buy or lease your car. It’s usually rolled into your car loan, so you don’t pay monthly but that means you’ll pay interest on it if it’s part of your financing. That can make it more expensive in the long run.

On the other hand, if you go through your insurance company, they may offer gap coverage as an add-on to your existing auto policy. This usually works out cheaper and more flexible because:

- You can remove it when you no longer need it.

- You’re not paying interest on it.

- You can shop around and compare prices easily.

So while dealerships are convenient (especially if you’re already there signing papers), insurance companies often give you more control and better pricing.

Do I have to pay monthly or can I pay all at once?

Good question! It depends on where you buy the gap insurance from.

If you buy it from your car dealer, you’ll likely pay it all at once but most of the time it’s included in your car loan. That means you’re paying for it slowly over time with interest. It feels easy, but you may end up paying more in the end without realizing it.

If you get it through your car insurance provider, you usually pay it monthly, just like your regular insurance premium. This keeps things simple and budget-friendly. You’ll see a small increase in your monthly bill maybe around $5 to $15 extra, depending on your car and coverage.

Bonus tip: Some companies let you cancel gap coverage mid-policy if you’ve paid off your loan enough and don’t need it anymore. That means you don’t waste money when the “gap” is gone.

Is Gap Insurance Worth It for You?

Now comes the big question: Should you even get gap insurance?

Well, it really depends on your car, your loan, and your situation. Let’s break it down in the easiest way possible.

When does gap insurance make sense and when it doesn’t

Gap insurance is super helpful when:

- You just bought a brand-new car, and its value will drop fast.

- You took out a big loan with little or no down payment.

- You’re leasing the car most lease companies require gap coverage.

- Your loan term is long, like 60+ months the longer the loan, the longer you might have a gap.

But gap insurance might not be needed if:

- You bought a used car that isn’t losing value quickly.

- You made a big down payment (so you don’t owe more than the car’s worth).

- You’ve already paid off most of your loan.

- Your car is almost fully paid or has a very small loan left.

Here’s a quick thought: If your car is worth more than or equal to what you owe, you don’t need gap insurance anymore simple as that.

Quick yes-or-no guide to decide if you need gap insurance

Let’s make this super easy. Just answer these:

- Did you buy or lease a new car in the last 12 months? → Yes? You probably need it.

- Did you put down less than 20% as a down payment? → Yes? You should consider it.

- Is your car loan more than 5 years (60 months)? → Yes? Gap insurance is smart.

- Did you roll other loans or fees into your car loan (like from an old car)? → Yes? Gap coverage is a good idea.

- Is your car already paid off or almost paid off? → Yes? You probably don’t need gap insurance.

If you answered “yes” to the first few, gap insurance can save you big money if something unexpected happens.